When you buy a home, you don't only buy the land, the house, and any other physical structures that come with it. The most important thing is that you are also buying the legal rights of ownership to the property, which is referred to as “title.”

This title is indicated in the “deed” — an official record of your rights and ownership of the property that states that it has been legally transferred to you by the previous owner. When you sell your home in the future, you will also transfer this rights to your buyer.

Before officially taking this title and completing the closing of the real estate transaction, a title search will be required to find any defects in the title. Chances are, there could be one or more issues that could emerge in the title. These title defects could cause you to lose your property, or make it impossible to you to sell when the time comes.

This type of insurance offers protection against any defects with the title or legal ownership status of a property. It covers financial loss from these problems or from any existing property liens. Title insurance may come in a bit hefty amount, but it is a one-time expense and does not carry with it additional monthly premiums. It will also cover the homeowner until the property is sold.

Is it worth it?

Because every property has a history, any defects in the title could hinder you from enjoying your ownership rights. However, having title insurance serves as your protection against possible title problems that may surface and could cause property loss or damage. Remember, any competing claim of ownership could seriously jeopardize your financial stake on your biggest investment. Because unfortunately, these problems may be discovered even after an initial title search was done on your property.

Title insurance is vital especially in purchasing rural property, since aside from any title claim, it will also advise you if the property has previously been used for non-residential purposes.

There are generally two types of title insurance coverage: a lender's title insurance and the owner’s policy. Most lenders require a buyer to purchase a lender’s policy as part of investor requirements. But this policy will not protect you but covers only the lender, hence its name.

It is the owner’s insurance policy that will protect your property — your biggest financial investment — against anyone who has a claim against your home.

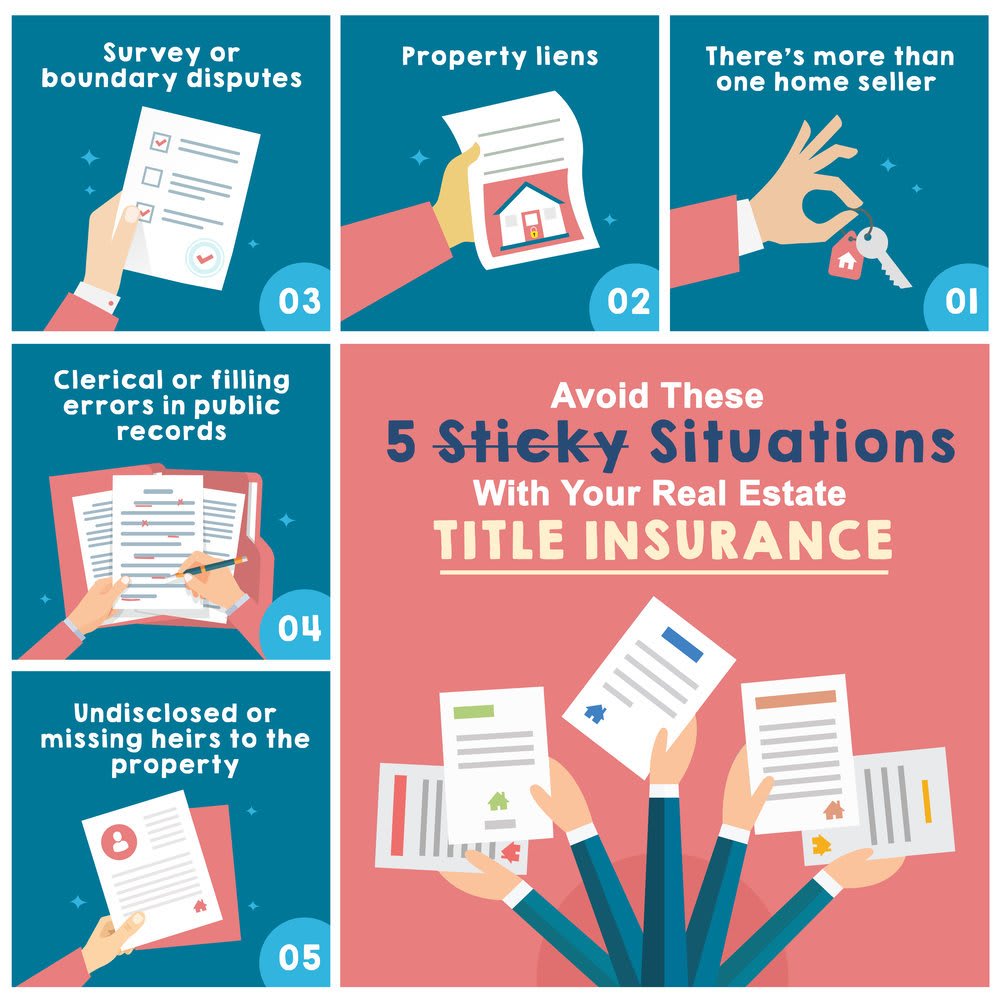

So you think you really own your property? Here are the most common title problems that could arise and dispute your rights to ownership:

1. There's more than one home seller (or homeowner)

At the time of your purchase, you may not know that there’s another seller or homeowner, maybe a relative or an ex-spouse. This third party may surface with a claim that they actually own all or a part of your property. They would insist that the seller had no right to sell the home to you in the first place.

In this situation, a judge could confirm and favor this third party’s claim to the house, which could leave you with a huge financial loss (and no home to live in). Fortunately, your own insurance policy could cover this loss. Your title insurance will pay for expenses such as attorney’s fees and court costs, while the lender’s insurance policy will pay for court costs incurred by the bank. The sale, on the other hand, will be deemed null and void.

2. Property liens for delinquent taxes, unpaid contractors, and other debts

There are circumstances where, unfortunately, the former homeowners were not diligent billpayers. This is worrisome because even if the debt is not your own, banks or other financing companies can place liens on your property to cover those unpaid debts.

These property liens can slow down the closing because your title won’t be considered clear until you pay the existing debt. Sometimes, even though a tax search hadn’t tracked down any unpaid taxes on the property, it’s still possible that you would get notified for any of these delinquent taxes after closing. It’s also a common issue if the property was foreclosed on or the home was bought in an online foreclosure auction website.

Fortunately, if you have an owner’s title insurance policy, it will cover for it and will give you documentation that the indicated debts are paid.

3. Survey or boundary disputes

Conflicts concerning the boundaries of your property may arise if, despite several surveys before closing, there are other existing surveys that show different property lines. This may lead to dispute especially when a neighbor or someone will claim ownership to a part of your property.

Likewise, if your neighbor happened to put up a fence or a driveway on a portion of your new property right before closing, you can count on your title insurance to settle the dispute. The policy will pay for the cost of any legal efforts to settle the issue out of court and have any of your neighbor’s item removed from it.

4. Clerical or filling errors in public records

When it comes to homeownership rights, a simple typo can lead to devastating title claim problems. These clerical errors in public records and/or courthouse documents could affect the deed or survey of your property. And while it isn’t impossible to resolve them, it can take an emotional and financial strain to any homeowner. Your title insurance serves as a cushion for this kind of problem.

5. Undisclosed or missing heirs to the property

Imagine this scenario: the former property owner died. So, the ownership of the home may fall to his heirs or to anyone indicated in his/her will. However, those heirs were missing or unknown at the time of his death, so the state sold the property, together with all of the assets.

When you purchase this kind of home, despite assuming the rights as the new owner, family members of the previous owner could come forward and claim ownership of the property. This claim could seriously jeopardize your rights to the home, even if it happens years after you bought the property.

Bottom Line

In these situations, the last thing any homebuyer or homeowner would want are hurdles that will cripple their ability to purchase the home and claim full ownership of it.

Even if there’s a slim chance that past owners or unpaid property tax bills might emerge, the risk is still huge considering what is at stake — your beloved home. If you are still contemplating whether you will allot money for it, just think how you will be affected if you’re suddenly faced with any of those title-related nightmares. Remember that you are entitled to choose the title company where you will get yours, so gather recommendations from your trusted real estate agent, lender, or family.